Executive Summary

Broadcom delivered a clean beat-and-raise anchored by accelerating AI semiconductors and a margin-rich VMware software base. Revenue rose 22% YoY to $15.95B, non-GAAP EPS hit $1.69, and FCF reached $7.0B (44% margin). Management guided Q4 revenue to ~$17.4B (+24% YoY) and disclosed AI semi revenue stepping from $5.2B in Q3 to $6.2B in Q4. The company also revealed >$10B of production orders from a new custom XPU customer and a consolidated backlog near $110B—plus Hock Tan staying as CEO through 2030. The result: Broadcom looks less like a cyclical “AI call option” and more like an AI operating model with multi-year visibility.

Results Snapshot: Quality of the Beat

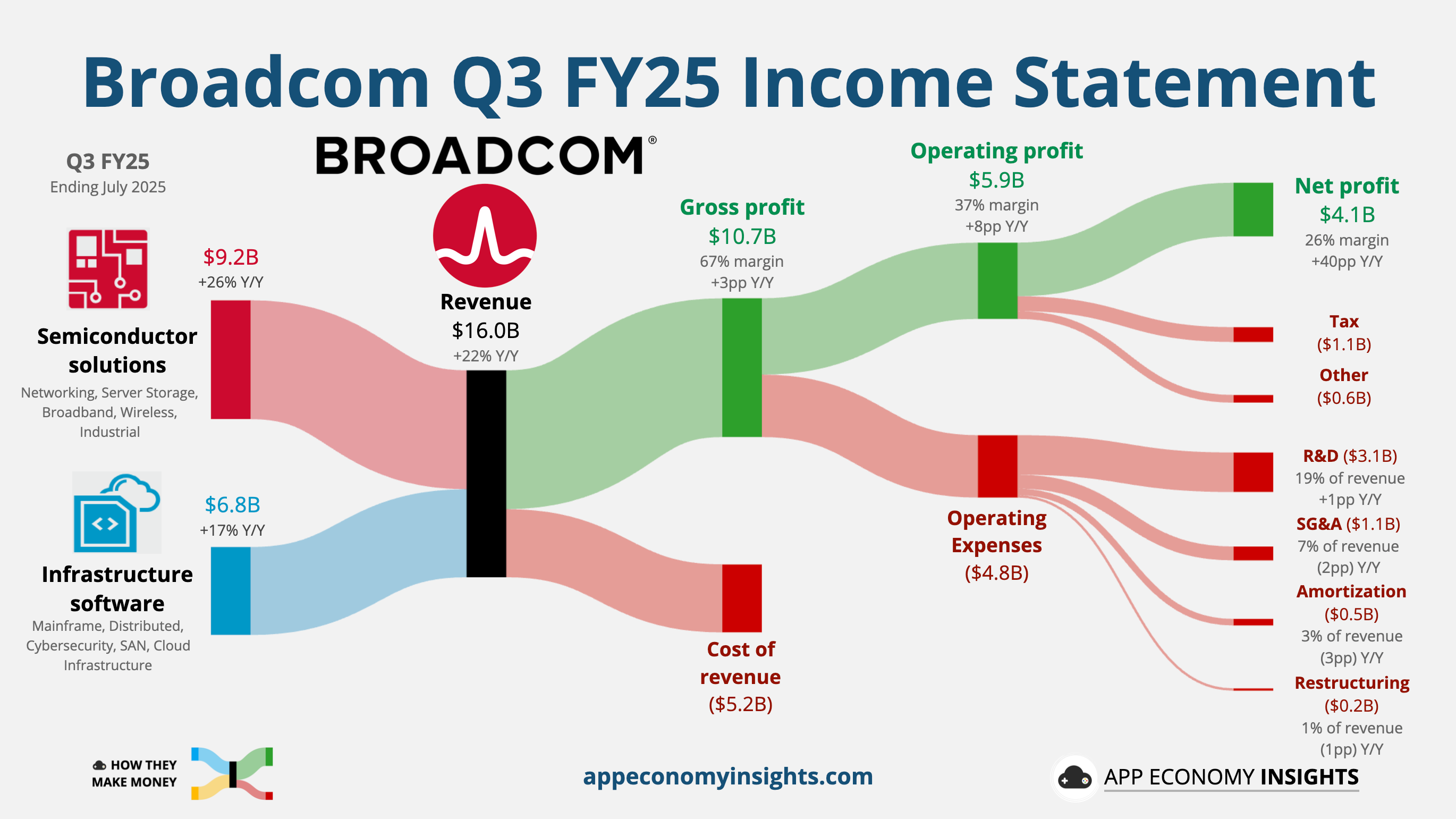

Revenue: $15,952M (+22% YoY).

Non-GAAP EPS: $1.69; Adj. EBITDA: $10,702M (67% margin).

Free cash flow: $7,024M (44% margin) on just $142M of capex → asset-light scale.

Dividend: $0.59/share; payable Sep 30, 2025 (record Sep 22).

Q4 guide: revenue ~$17.4B; Adj. EBITDA ~67%.

Mix matters:

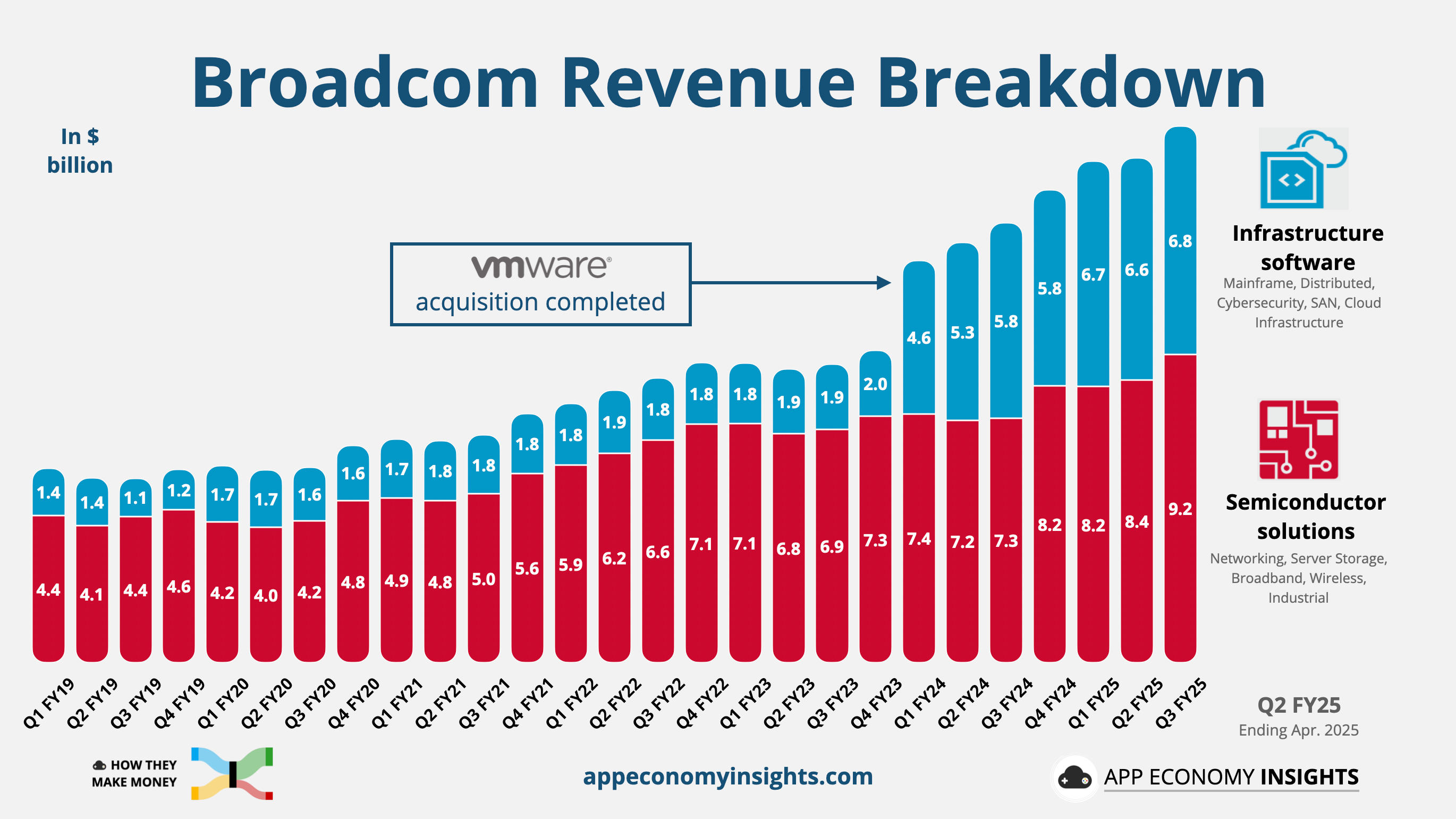

Semiconductor Solutions: $9.17B (+26% YoY; 57% of total).

Infrastructure Software (incl. VMware): $6.79B (+17% YoY; 43%).

AI Semiconductors: The XPU + Ethernet Playbook Is Working

Run rate and mix. AI semiconductor revenue printed $5.2B in Q3 (+63% YoY) and is guided to $6.2B in Q4 (+66% YoY). Within AI, custom XPUs now account for ~65%—a powerful margin-and-share lever as hyperscalers pursue cost control and architectural independence. The new qualified XPU customer placed >$10B of orders for AI racks, with management explicitly tying that to stronger FY26 AI growth. Street reporting widely infers OpenAI as the unnamed buyer, though Broadcom did not identify the customer.

Networking advantage. Broadcom pressed its case for Open Ethernet at massive cluster scale. The company highlighted Tomahawk 6 (102T), enabling a two-tier fabric (vs. three tiers at 51.2T), reducing latency and power at scale—critical as customers push beyond 100k compute nodes. This is a secular Ethernet share-gain story in AI data centers, not a one-off product cycle.

Why this matters:

Diversification vs GPUs. Custom XPUs + Ethernet fabrics let hyperscalers blunt supply/cost constraints of off-the-shelf GPUs and drive TCO lower.

Durability of demand. The new XPU order, combined with an ~$110B backlog, extends visibility into 2026 and reduces the risk that current AI spending is transient.

Infrastructure Software (VMware): Margin Machine, AI Enabler

Performance and profitability. VMware-led Infrastructure Software delivered $6.8B (+17% YoY) with ~93% gross margin and ~77% operating margin, reflecting integration efficiencies and portfolio focus. Management guides ~$6.7B for Q4 (+15% YoY), underscoring steady, high-margin cash generation.

Strategic role. Beyond P&L accretion, VMware is a control point for private/hybrid compute—where many enterprises will deploy inference securely. Broadcom’s ability to bundle networking silicon, DPUs, and VMware stack elements should support attach rates and pricing power, even if non-AI semis take longer to recover cyclically.

Margins, Mix & Cash: Reading the Signals

Consolidated gross margin: 78.4% in Q3. For Q4, management guides ~70 bps lower sequentially on higher XPU and seasonal wireless mix. That headwind is tactical, not structural, given software’s stabilizing effect and semi operating leverage.

FCF engine: $7.0B FCF on $16.0B revenue and $142M capex reiterates the asset-light nature of Broadcom’s model amid an AI ramp largely funded on the customer side.

Balance sheet: $10.7B cash; $66.3B gross debt (fixed-rate $65.8B with 3.9% coupon; 6.9 years WAM). Manageable maturity profile supports dividends and selective inorganic moves.

What Changed vs. Last Quarter

The scale of AI visibility improved. The >$10B new XPU order plus commentary that FY26 AI revenue should improve significantly marks a step-function in backlog quality. External coverage ties the scale/timing to OpenAI, which—if accurate—adds another blue-chip anchor alongside existing hyperscaler relationships.

The networking roadmap was clarified. The move to 102T and two-tier fabrics strengthens the case that Ethernet’s time in AI has arrived, compressing latency/power and broadening vendor optionality at rack and cluster scale.

Software synergy was realized. VMware margins (93% gross / 77% op) show Broadcom has crossed the tough part of integration; the Q4 guide implies sustainability rather than a one-time step-up.

Outlook & Scenario Framing (Next 12–18 Months)

For Q4 FY25, the guidance indicates approximately $17.4 billion in revenue and an adjusted EBITDA of around 67%, with AI semiconductor revenue projected at $6.2 billion. Expect a gross margin of ~70 bps QoQ on mix.

FY26 (qualitative): Management indicates meaningfully higher AI revenue vs. prior view, underpinned by the new XPU program. External analysts (e.g., Bernstein via Reuters) suggest AI sales could top prior $30B expectations for FY26.

Key swing factors to monitor

Ramp cadence of the new XPU customer (tape-outs, yields, packaging, and rack-level integration).

Ethernet cluster deployments at 102T and optics availability—gatekeepers for very large cluster performance.

Enterprise budgets for on-prem/private AI that pull VMware along with networking and DPUs.

Risks & Offsets

Customer concentration/architectural shifts. Hyperscaler spending is powerful but can be lumpy; any pivot in accelerator roadmaps or in-house design cadence could alter ramps. Offset: multi-customer XPU portfolio + Ethernet share gains.

Mix-driven margin compression. Higher XPU (vs networking/software) can pressure GMs sequentially. Offset: software margins and scale economics in custom silicon.

Macro & supply chain. The lead times for cutting-edge switches and optics, as well as the packaging capacity, continue to be important items to monitor.

30–90 Day Watchlist (Actionable Follow-Ups)

Customer disclosures/ecosystem press that triangulate the new XPU program (vendors, packaging partners, optical interconnects).

Investor events / fireside chats for incremental FY26 color (AI semi split: XPU vs. Ethernet; non-AI semi stabilization).

VMware renewals & SKU mix as subscription migration matures; look for indicators of attachment to AI-adjacent private cloud builds.

Disclaimer: This article is provided for informational and analytical purposes only and does not constitute investment advice or a recommendation to buy or sell any financial instrument. The views expressed are those of the author, based on sources deemed reliable at the time of writing, and are subject to change without notice. We make no guarantees about the information's accuracy, completeness, or timeliness, and we are not liable for any losses from its use. Before making any investment decision, you should consult a qualified professional to assess your individual objectives, risk tolerance, and financial circumstances.

Thank you, Mike, for the excellent analysis and insights.